Top 10 Brilliant Money Saving Tips 2026: महंगाई के जमाने में पैसा बचाने के 10 सीक्रेट तरीके!

Top 10 Brilliant Money Saving Tips 2026: Dosto, आज के दौर में पैसा कमाना जितना मुश्किल है, उससे कहीं ज्यादा मुश्किल उसे बचाना (Save) है। 2026 में जैसे-जैसे महंगाई (Inflation) बढ़ रही है, अगर आपका Financial Planning सही नहीं है, तो महीने की 20 तारीख तक हाथ खाली हो जाता है।

अमीर वो नहीं होता जो बहुत ज्यादा कमाता है, अमीर वो होता है जिसे Paisa Bachana आता है। इस ब्लॉग में हम बात करेंगे Top 10 Brilliant Money Saving Tips 2026 की, जो आपकी सेविंग्स को रॉकेट की तरह बढ़ा देंगी।

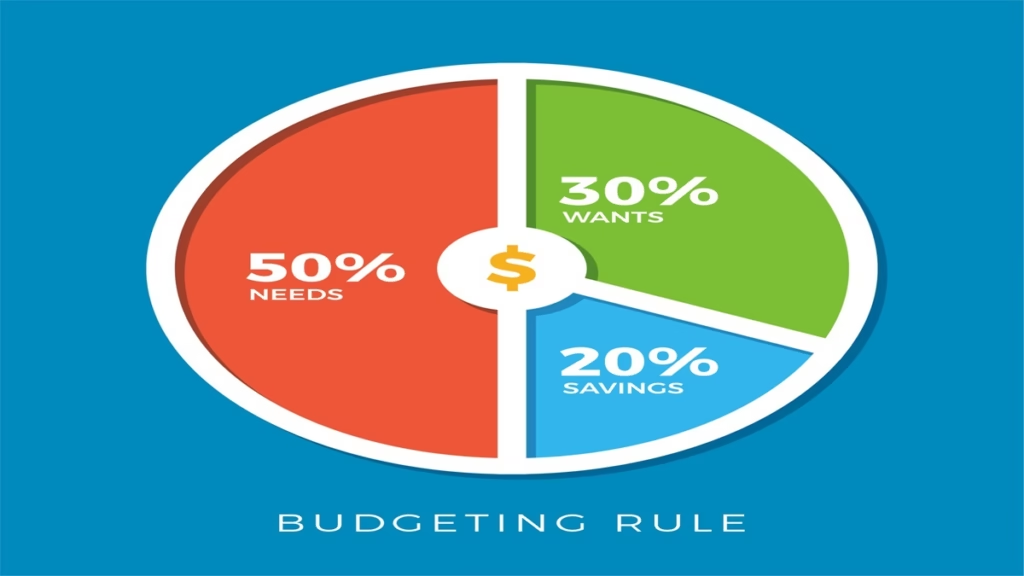

1. 50/30/20 Rule को फॉलो करें

Top 10 Brilliant Money Saving Tips 2026: यह बजटिंग का सबसे पावरफुल नियम है। अपनी इन-हैंड सैलरी को तीन हिस्सों में बांटें:

- 50%: Needs (जरूरतें जैसे किराया, राशन, बिजली बिल)।

- 30%: Wants (इच्छाएं जैसे बाहर खाना, मूवी, नेटफ्लिक्स)।

- 20%: Savings & Investment (यह हिस्सा सबसे पहले अलग करें)।

2. Subscriptions का ऑडिट करें

Top 10 Brilliant Money Saving Tips 2026: हम अक्सर Netflix, Hotstar, Gym या किसी App का सब्सक्रिप्शन लेकर भूल जाते हैं। 2026 में डिजिटल खर्च बहुत बढ़ गया है। अपनी बैंक स्टेटमेंट चेक करें और जो सर्विस आप इस्तेमाल नहीं कर रहे, उसे तुरंत Cancel करें।

3. ’24-Hour Rule’ अपनाएं

Top 10 Brilliant Money Saving Tips 2026: जब भी आपका मन कोई महंगी चीज खरीदने का करे (जैसे नया फोन या कपड़े), तो तुरंत ऑर्डर न करें। कम से कम 24 घंटे इंतज़ार करें। आप पाएंगे कि अगले दिन तक वो चीज खरीदने की इच्छा 70% कम हो चुकी होगी। यह ‘Impulse Buying’ रोकने का बेस्ट तरीका है।

4. Savings को Automate करें

Top 10 Brilliant Money Saving Tips 2026: इंसानी दिमाग खर्च करने के बहाने ढूंढ लेता है। इसलिए अपनी SIP (Systematic Investment Plan) या RD की तारीख महीने की 1 से 5 के बीच रखें। पैसा हाथ में आने से पहले ही इन्वेस्ट हो जाएगा, तो खर्च करने का मौका ही नहीं मिलेगा।

5. UPI के बजाय Cash का इस्तेमाल करें

Top 10 Brilliant Money Saving Tips 2026: Digital India के दौर में UPI ने खर्च करना बहुत आसान बना दिया है, जिससे हमें पता ही नहीं चलता कि पैसे कहाँ उड़ गए। छोटे खर्चों (सब्जी, दूध, चाय) के लिए कैश इस्तेमाल करें। जब जेब से नोट कम होते हैं, तो दिमाग अपने आप अलर्ट हो जाता है।

6. Electricity और Fuel बचाएं

Top 10 Brilliant Money Saving Tips 2026: 2026 में बिजली और पेट्रोल के दाम आसमान छू रहे हैं। अगर मुमकिन हो तो EV (Electric Vehicle) या पब्लिक ट्रांसपोर्ट का इस्तेमाल करें। घर में LED बल्ब और स्टार-रेटेड अप्लायंसेज लगाएं। ये छोटे बदलाव साल के अंत में बड़ी बचत करते हैं।

7. Generic Medicines खरीदें

Top 10 Brilliant Money Saving Tips 2026: हेल्थ का खर्चा कभी भी आ सकता है। महंगी ब्रांडेड दवाओं के बजाय Generic Medicines चुनें। इनमें साल्ट वही होता है लेकिन कीमत 50% से 80% तक कम होती है। बस अपने डॉक्टर से एक बार सलाह जरूर लें।

8. Grocery Shopping की लिस्ट बनाएं

Top 10 Brilliant Money Saving Tips 2026: कभी भी खाली पेट या बिना लिस्ट के सुपरमार्केट न जाएं। बिना लिस्ट के जाने पर हम वो चीजें भी उठा लेते हैं जिनकी जरूरत नहीं होती। हमेशा भारी डिस्काउंट वाले ‘Bulk Packs’ तभी लें जब उस सामान की वाकई जरूरत हो।

9. Cooking at Home (No More Zomato/Swiggy)

Top 10 Brilliant Money Saving Tips 2026: बाहर से खाना मंगाने पर फूड कॉस्ट के साथ-साथ डिलीवरी चार्ज और टैक्स भी देना पड़ता है। हफ्ते में सिर्फ एक बार बाहर खाने का नियम बनाएं। घर का बना खाना न सिर्फ सस्ता होता है, बल्कि सेहत के लिए भी बेस्ट है।

10. Financial Literacy पर ध्यान दें

Top 10 Brilliant Money Saving Tips 2026: पैसे बचाकर उसे बैंक अकाउंट में छोड़ देना समझदारी नहीं है। 2026 में आपको Mutual Funds, Index Funds या Stocks के बारे में सीखना चाहिए। जब आपका पैसा ‘Compounding’ के जरिए बढ़ेगा, तभी आप सही मायने में पैसे बचा पाएंगे।

Conclusion: आज से ही शुरुआत करें!

Top 10 Brilliant Money Saving Tips 2026: पैसे बचाना एक आदत है (Saving is a habit)। ऊपर दी गई Top 10 Brilliant Money Saving Tips 2026 को अगर आप अपनी लाइफ में उतारते हैं, तो अगले 1 साल में आप अपने बैंक बैलेंस में बड़ा अंतर देखेंगे। याद रखिए, “A penny saved is a penny earned.”

Quick Saving Table for 2026

| Tip | Expected Saving (Monthly) |

| Audit Subscriptions | ₹500 – ₹2000 |

| Home Cooking | ₹3000 – ₹5000 |

| 24-Hour Rule | ₹2000 – ₹10,000 |

| Electricity/Fuel Saving | ₹1000 – ₹3000 |

Top 10 Brilliant Money Saving Tips 2026 – Save ₹10,000+ Every Month

Introduction: The 2026 Financial Landscape

Top 10 Brilliant Money Saving Tips 2026: As we step into 2026, the economic landscape continues to evolve with new challenges and opportunities. Inflation, technological advancements, and shifting consumer habits require smarter approaches to personal finance. The good news? With strategic planning and modern tools, saving ₹10,000 or more every month is not just possible but achievable for most households. This comprehensive guide presents ten brilliant, practical strategies tailored for the financial realities of 2026, combining traditional wisdom with cutting-edge approaches.

Top 10 Brilliant Money Saving Tips

1. AI-Powered Expense Optimization

The Future of Spending Analysis

Artificial Intelligence has transformed from a buzzword to a practical daily tool. In 2024, nearly 45% of banking apps incorporated some form of AI spending analysis. By 2026, this is expected to exceed 80%.

Implementation Strategy

Step 1: Choose an AI-powered financial aggregator app that connects to all your accounts. Look for features like predictive spending alerts, automated categorization, and personalized saving suggestions.

Step 2: Allow the AI to analyze your spending patterns for one full billing cycle without making changes. The system will identify “leakage points”—those recurring subscriptions you forgot about, impulse purchases, or inefficient spending patterns.

Step 3: Implement the AI’s top three recommendations each month. A typical AI analysis can identify ₹2,000-₹4,000 in unnecessary monthly expenses for the average urban household.

Monthly Saving Potential: ₹2,000-₹4,000

2. The 2026 Subscription Audit Revolution

The Subscription Economy Problem

The average Indian household now has 12.7 active subscriptions across entertainment, software, food delivery, and wellness services. Many are underutilized or completely forgotten.

Implementation Strategy

Digital Detox Day: Designate one day quarterly as your subscription audit day. Use apps like Truebill or native banking tools that identify recurring charges.

The 90-Day Rule: Any subscription not used in 90 days gets cancelled immediately. For borderline cases, implement the “one-month pause” to test if you truly miss the service.

Family Subscription Pooling: Coordinate with extended family or trusted friends to share subscriptions legally. Many services now offer family plans covering 4-6 users at 40-60% savings per person.

Monthly Saving Potential: ₹1,500-₹3,000

3. Smart Grocery 3.0: Beyond Coupons

The Data-Driven Kitchen

Grocery costs have risen approximately 22% since 2021, making this category one of the largest household expenses.

Implementation Strategy

AI Meal Planning: Use apps that create weekly meal plans based on sale items at your preferred stores, minimizing waste and maximizing nutritional value.

Dynamic Shopping Lists: Implement smart lists that adjust based on your consumption patterns and current pantry inventory.

Bulk-Buy Intelligence: Use price tracking tools to identify when staples hit their annual low prices. Combine this with cashback credit cards (paid in full monthly) for additional savings.

Monthly Saving Potential: ₹2,000-₹3,500

4. The Mobility Transformation

Rethinking Transportation in 2026

With fuel prices fluctuating and new mobility options emerging, transportation requires a hybrid approach.

Implementation Strategy

Electric Vehicle Subsidy Maximization: If considering a vehicle purchase, explore the enhanced 2026 EV subsidies and calculate total cost of ownership against conventional vehicles.

Micro-Mobility Integration: For urban dwellers, combine walking, cycling, e-scooters, and public transit using mobility-as-a-service apps that find the cheapest combination for each journey.

Telecommuting Tax Benefits: If you work from home regularly, ensure you’re claiming all eligible deductions for home office expenses, which have expanded in 2026.

Monthly Saving Potential: ₹1,000-₹2,500

5. Energy Intelligence Systems

Home Energy Management

Energy costs continue to rise, but smart home technology offers unprecedented control.

Implementation Strategy

Smart Thermostat Optimization: These devices now learn your patterns and adjust automatically, typically saving 10-15% on heating and cooling.

Peak Load Shaving: Use energy monitoring systems to identify when your utility charges peak rates and program high-consumption devices (like washing machines) to run during off-peak hours.

Monthly Saving Potential: ₹800-₹1,800

6. Healthcare Financial Optimization

Proactive Health Finance

Medical costs are increasingly predictable with proper planning.

Implementation Strategy

Preventive Care Maximization: Utilize all covered preventive services, which are typically 100% covered by insurance and can prevent costly treatments later.

Telemedicine First: For non-emergency issues, telemedicine consultations cost 40-70% less than in-person visits with similar outcomes for many conditions.

Generic Medication Automation: Use apps that automatically find the lowest pharmacy prices for your medications and provide manufacturer coupons.

Monthly Saving Potential: ₹600-₹1,500

7. Digital Upskilling for Income Augmentation

The Side-Hustle Evolution

The gig economy has matured into specialized digital services with higher earning potential.

Implementation Strategy

Micro-Certification Paths: Identify 2-3 high-demand digital skills in your field (like data visualization, AI prompt engineering, or cybersecurity basics) and complete certified micro-courses.

Platform Specialization: Rather than general freelancing, specialize in a specific platform (Shopify optimization, WordPress security, etc.) where you can charge premium rates.

Time-Blocking for Side Income: Dedicate 5-7 hours weekly to your income augmentation activities, treating this time as non-negotiable.

Monthly Earning Potential: ₹3,000-₹8,000 (additional income, not savings, but contributing to the ₹10,000+ goal)

8. Smart Debt Management 2026

Interest Rate Optimization

New tools make debt restructuring more accessible than ever.

Implementation Strategy

Automatic Refinancing Monitors: Use services that continuously scan for better loan rates and automatically initiate refinancing when beneficial.

Debt Avalanche 2.0: Apps now visualize different payoff strategies and automatically allocate extra payments to the optimal debt.

Monthly Saving Potential: ₹1,200-₹2,500 (from reduced interest payments)

9. Conscious Consumption & Circular Economy Participation

Value Retention Mindset

The resale and refurbishment markets have grown exponentially, creating opportunities for savers.

Implementation Strategy

One-In-Two-Out Rule: For every new non-essential item brought in, two similar items must be sold or donated.

Rental Economy Participation: For infrequently used items (power tools, specialty clothing, camping equipment), join rental platforms rather than purchasing.

Monthly Saving Potential: ₹1,000-₹2,200

10. Future-Proof Financial Automation

The Set-and-Forget System

Advanced automation ensures savings happen without willpower depletion.

Implementation Strategy

Round-Up Investment Portfolios: Apps that round up purchases to the nearest ₹10 and invest the difference in diversified portfolios have evolved to include tax optimization.

Dynamic Emergency Fund: Instead of a static emergency fund, use algorithms that adjust your cash holdings based on economic indicators and personal risk factors.

Goal-Based Bucket Systems: Automate transfers to specific goal accounts (vacation, car replacement, home renovation) with visual tracking systems.

Monthly Saving Potential: ₹800-₹1,500 (from automated systems that prevent spending)

Implementation Timeline: Your 90-Day Plan

Weeks 1-2: Setup Phase

- Implement AI expense tracker and automation systems

- Conduct complete subscription audit

- Set up all necessary apps and accounts

Weeks 3-8: Optimization Phase

- Week 3-4: Focus on groceries and utilities

- Week 5-6: Implement transportation and healthcare changes

- Week 7-8: Begin debt optimization and circular economy practices

Weeks 9-12: Income Augmentation Phase

- Begin digital upskilling course

- Establish side-income time blocks

- Refine all systems based on initial results

Potential Challenges and Solutions

Challenge 1: Data privacy concerns with financial apps

Solution: Use apps with local processing, strong encryption, and clear data policies. Many Indian fintech apps now offer on-device AI processing.

Challenge 2: Family resistance to lifestyle changes

Solution: Implement changes gradually and involve all household members in goal setting. Use visual progress trackers and celebrate milestones.

Challenge 3: Analysis paralysis from too many options

Solution: Start with just three strategies from this list that resonate most with your situation. Add one new strategy each month.

Conclusion: Financial Freedom in 2026

Saving ₹10,000+ monthly in 2026 requires neither extreme frugality nor exceptional income. It demands intelligent system design, leveraging technology, and consistent small optimizations across spending categories. The strategies outlined here work synergistically—each reinforcing the others to create substantial cumulative savings.

The most important step is to begin. Select one strategy that seems most accessible and implement it this week. As you experience the psychological and financial benefits, you’ll gain momentum to incorporate additional strategies. By this time next year, you could have an extra ₹1.2 lakhs or more working for your future rather than disappearing into inefficient spending patterns.

Remember: Wealth in 2026 isn’t just about earning more—it’s about optimizing what flows through your hands. Start your journey today.

Frequently Asked Questions (FAQs)

Q1: I’ve tried budgeting apps before and failed. Why will AI-powered tools be different in 2026?

A: Earlier budgeting tools required significant manual input and categorization. 2026’s AI tools use natural language processing to automatically understand transactions, predictive analytics to forecast cash flow, and personalized nudges that adapt to your behavioral patterns. They’re less about tracking and more about intelligent prevention of wasteful spending before it happens.

Q2: Are these strategies realistic for someone earning ₹30,000-₹40,000 per month?

A: Absolutely. The strategies are scalable. Someone earning ₹35,000 might save ₹3,000 through subscription optimization and grocery planning, another ₹2,000 through transportation changes, and generate ₹3,000 through side-income activities. The key is focusing on percentage savings rather than absolute amounts and prioritizing strategies that match your lifestyle.

Q3: How much time will maintaining these systems require weekly?

A: After the initial setup (4-6 hours), most systems run automatically. The weekly commitment is approximately 30-45 minutes for review and minor adjustments. Digital upskilling requires additional dedicated time (5-7 hours weekly if pursuing income augmentation), but this is an investment that increases earning potential long-term.

Q4: What if my spouse/family isn’t onboard with these changes?

A: Start with “win-win” strategies that don’t feel restrictive. AI grocery optimization often means better meals for less money. Subscription audits frequently reveal services nobody is using. Share progress visually—when family members see the vacation fund growing or debt decreasing, they typically become more engaged.

Q5: How do I prioritize which strategies to implement first?

A: Begin with a 30-day spending analysis (automated by AI tools) to identify your largest “leakage points.” Most people find immediate wins in subscription optimization (Strategy #2) and grocery planning (Strategy #3). Implement these first, then add one new strategy each month. The psychological boost from early successes creates momentum for more challenging behavioral changes.

Disclaimer: The information provided is for educational purposes. Individual results may vary based on personal circumstances, location, and economic factors.

Consider consulting with a certified financial planner for

personalized advice tailored to your specific situation.