Loan Vs Credit Card Apply Decision: कर्ज घ्यावे की क्रेडिट कार्ड? योग्य आर्थिक निर्णय घेण्यासाठी ही सविस्तर मार्गदर्शिका वाचा!

Loan Vs Credit Card Apply Decision: आयुष्यात कधी ना कधी आपल्याला अतिरिक्त पैशांची गरज भासते—मग ते मुलांच्या शिक्षणासाठी असो, घराच्या नूतनीकरणासाठी असो किंवा एखादी मोठी खरेदी करण्यासाठी. अशा वेळी आपल्यासमोर दोन मुख्य पर्याय उभे राहतात: पर्सनल लोन (Personal Loan) किंवा क्रेडिट कार्ड (Credit Card).

अनेकजण घाईघाईत चुकीचा पर्याय निवडतात आणि नंतर जास्तीच्या व्याजाच्या विळख्यात अडकतात. तुमच्यासाठी कोणता पर्याय सर्वोत्तम आहे? चला, Loan Vs Credit Card Apply Decision घेताना कोणत्या गोष्टी लक्षात ठेवाव्यात, हे सविस्तर पाहूया.

१. वैयक्तिक कर्ज (Personal Loan) कधी निवडावे?

Loan Vs Credit Card Apply Decision: पर्सनल लोन हे मोठ्या खर्चासाठी आणि दीर्घकाळासाठी सर्वोत्तम मानले जाते.

- केव्हा घ्यावे: लग्नाचा खर्च, घराचे नूतनीकरण, किंवा जुन्या कर्जांची फेड (Debt Consolidation) करण्यासाठी.

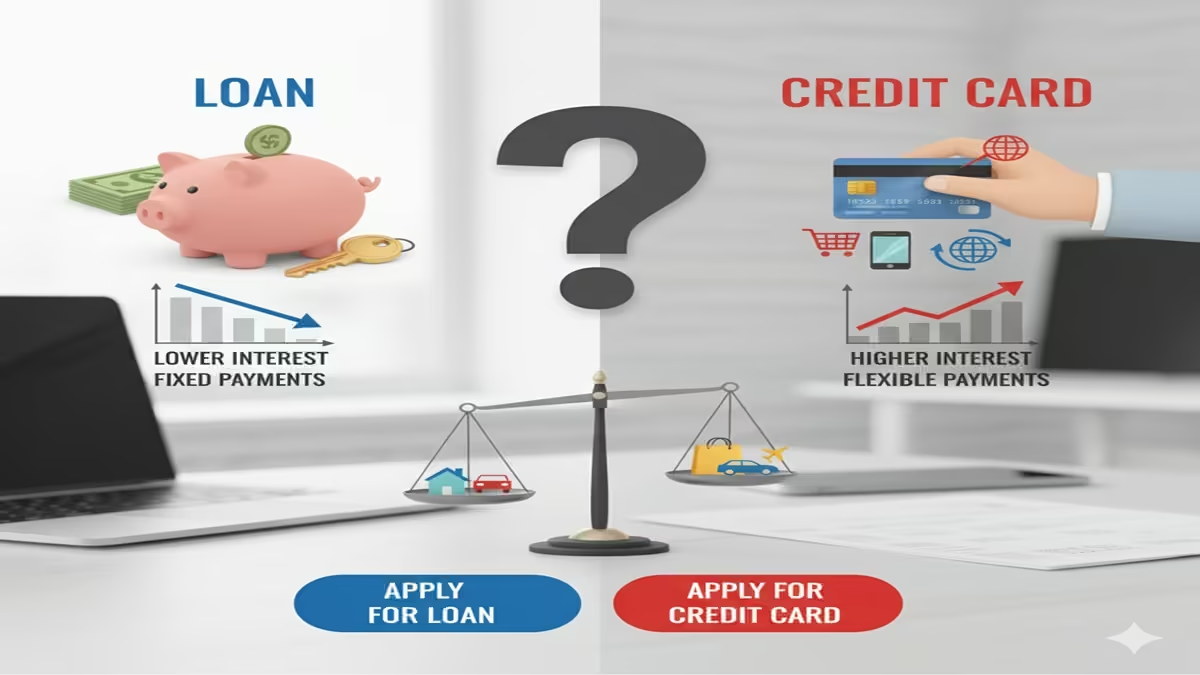

- व्याजदर: याचा व्याजदर स्थिर असतो आणि साधारणपणे क्रेडिट कार्डपेक्षा कमी (१०% ते १५%) असतो.

- कालावधी: तुम्ही १ ते ५ वर्षांच्या कालावधीसाठी हे कर्ज घेऊ शकता.

- फायदा: तुम्हाला एकदम मोठी रक्कम मिळते आणि दरमहा ठराविक हप्ता (EMI) भरावा लागतो, ज्यामुळे बजेट नियोजन सोपे होते.

२. क्रेडिट कार्ड (Credit Card) कधी निवडावे?

Loan Vs Credit Card Apply Decision: क्रेडिट कार्ड हे प्रामुख्याने दैनंदिन खर्च आणि आपत्कालीन परिस्थितीसाठी असते.

- केव्हा घ्यावे: ग्रोसरी शॉपिंग, ऑनलाईन खरेदी, प्रवासाचे तिकीट बुक करणे किंवा छोटी तातडीची गरज असल्यास.

- व्याजदर: जर तुम्ही वेळेवर बिल भरले नाही, तर व्याजाचा दर अत्यंत जास्त (३०% ते ४५% वार्षिक) असू शकतो. मात्र, ‘Interest-Free’ पिरीयडमध्ये वापरल्यास हे मोफत पडते.

- फायदा: रिवॉर्ड पॉइंट्स, कॅशबॅक आणि एअरपोर्ट लाउंज ॲक्सेस यांसारखे अतिरिक्त फायदे मिळतात.

३. निवडीसाठी ५ सुवर्ण नियम (Decision Matrix)

Loan Vs Credit Card Apply Decision: योग्य निर्णय घेण्यासाठी खालील मुद्द्यांचा विचार करा:

- गरज किती मोठी आहे? जर तुम्हाला ₹२ लाखांपेक्षा जास्त रक्कम हवी असेल, तर पर्सनल लोन घ्या. ₹५०,००० पेक्षा कमी रकमेसाठी क्रेडिट कार्ड सोयीचे आहे.

- परतफेडीचा कालावधी: जर तुम्ही ३-४ महिन्यात पैसे परत करू शकत असाल, तर क्रेडिट कार्ड वापरा. जर तुम्हाला १-२ वर्षांचा वेळ हवा असेल, तर लोन स्वस्त पडेल.

- व्याजदर: क्रेडिट कार्डवर वेळेवर पैसे न भरल्यास चक्रवाढ व्याज लागते, जे कर्जापेक्षा खूप जास्त असते.

- क्रेडिट स्कोअर: दोन्ही पर्यायांचा तुमच्या सिबिल (CIBIL) स्कोअरवर परिणाम होतो. क्रेडिट कार्डचे लिमिट जास्त वापरल्यास स्कोअर कमी होऊ शकतो, तर लोनचे हप्ते वेळेवर भरल्यास स्कोअर सुधारतो.

- प्रोसेसिंग फी: लोनसाठी १-२% प्रोसेसिंग फी द्यावी लागते, तर क्रेडिट कार्डसाठी जॉइनिंग फी असू शकते किंवा नसू शकते.

४. Loan Vs Credit Card: मुख्य फरक (Comparison Table)

| वैशिष्ट्य | पर्सनल लोन (Personal Loan) | क्रेडिट कार्ड (Credit Card) |

| व्याजदर | कमी (१०% – १५%) | जास्त (३०% – ४५% – जर बिल थकले तर) |

| वापर | एकदाच मोठी रक्कम | पुन्हा पुन्हा वापरता येते |

| मंजुरी वेळ | २४ ते ४८ तास | एकदा कार्ड मिळाले की त्वरित |

| कालावधी | १ ते ५ वर्षे | मासिक चक्र (Monthly Cycle) |

| लवचिकता | कमी (ठराविक EMI) | जास्त (खर्च तुमच्या हातात) |

५. २०२६ मधील नवीन ट्रेंड्स

Loan Vs Credit Card Apply Decision: आता बँका ‘Pre-approved Loans’ क्रेडिट कार्डवरच देत आहेत. जर तुम्हाला तुमच्या क्रेडिट कार्डवर कमी व्याजात लोन मिळत असेल, तर तो एक उत्तम मध्यम मार्ग ठरू शकतो.

निष्कर्ष (Conclusion)

Loan Vs Credit Card Apply Decision हा पूर्णपणे तुमच्या सध्याच्या आर्थिक स्थितीवर आणि गरजेवर अवलंबून असतो. जर तुम्हाला ‘डिसीप्लीन’ पद्धतीने खर्च करता येत असेल आणि पैसे लवकर परत करण्याची खात्री असेल, तर क्रेडिट कार्ड उत्तम आहे. परंतु, मोठ्या आणि लांब पल्ल्याच्या नियोजनासाठी पर्सनल लोन हाच सुरक्षित आणि स्वस्त पर्याय ठरतो.

Loan vs. Credit Card: A Comprehensive Guide to Making the Right Financial Decision

Introduction

Loan Vs Credit Card Apply Decision In today’s financial landscape, consumers have more options than ever when they need access to funds. Two of the most common solutions—personal loans and credit cards—serve similar purposes but operate under fundamentally different structures. Whether you’re consolidating debt, financing a major purchase, or covering unexpected expenses, choosing between a loan and a credit card can significantly impact your financial health for years to come.

Loan Vs Credit Card Apply Decision: The decision isn’t always straightforward. Each option carries distinct advantages, drawbacks, and ideal use cases that vary based on individual circumstances. This comprehensive guide will explore the intricate details of both financial tools, providing you with the knowledge to make an informed decision aligned with your financial goals.

Understanding Personal Loans: Structure and Mechanics

What is a Personal Loan?

Loan Vs Credit Card Apply Decision: A personal loan is a lump-sum amount of money borrowed from a financial institution—such as a bank, credit union, or online lender—that is repaid with interest over a fixed period. These loans are typically unsecured, meaning they don’t require collateral, though secured options exist for those with poor credit or seeking lower rates.

Key Characteristics of Personal Loans:

- Fixed Amount and Terms: You receive the entire loan amount upfront and repay it through equal monthly installments over a predetermined period, usually ranging from 12 to 84 months.

- Fixed Interest Rates: Most personal loans come with fixed interest rates, providing predictability in monthly payments throughout the loan term.

- Structured Repayment Schedule: From day one, you know exactly how much you’ll pay each month and when the debt will be fully repaid.

- Origination Fees: Many lenders charge an upfront fee (typically 1-8% of the loan amount) for processing the loan, which is either deducted from the disbursed amount or added to the total balance.

- Credit Requirements: Personal loans generally require good to excellent credit (typically FICO scores of 660+) for the most favorable terms, though some lenders specialize in serving borrowers with lower scores.

Ideal Use Cases for Personal Loans:

- Debt Consolidation: Combining multiple high-interest debts into a single loan with a lower interest rate

- Major Purchases: Financing significant expenses like home renovations, weddings, or medical procedures

- Unexpected Large Expenses: Covering emergency costs that exceed typical savings

- Credit Building: Establishing a positive payment history through structured repayment

Understanding Credit Cards: Flexibility and Revolving Credit

What is a Credit Card?

Loan Vs Credit Card Apply Decision: A credit card provides a revolving line of credit that can be borrowed against repeatedly up to a predetermined limit. Unlike a loan, you’re not receiving a lump sum but rather access to funds that can be used as needed, with the balance fluctuating based on purchases and payments.

Key Characteristics of Credit Cards:

- Revolving Credit: As you pay down your balance, that credit becomes available to use again, creating a continuous borrowing cycle.

- Variable Interest Rates: Most credit cards have variable APRs that can change with market conditions, though some offer introductory fixed rates.

- Minimum Payments: Card issuers require only a minimum payment each month (typically 1-3% of the balance), though paying only the minimum extends the repayment period and increases interest costs dramatically.

- Additional Features: Credit cards often come with rewards programs, purchase protections, travel benefits, and other perks not typically associated with personal loans.

- Accessibility: While premium cards require excellent credit, options exist for virtually all credit profiles, including secured cards for those building or rebuilding credit.

Ideal Use Cases for Credit Cards:

- Everyday Purchases: Convenient payment method for daily expenses

- Building Credit History: Regular use and timely payments demonstrate creditworthiness

- Emergency Funding: Immediate access to funds in urgent situations

- Rewards Optimization: Earning cash back, points, or miles on routine spending

- Purchase Protection: Taking advantage of fraud protection, extended warranties, and dispute resolution services

Comparative Analysis: Loans vs. Credit Cards

Interest Rates and Cost Implications

Loan Vs Credit Card Apply Decision: Personal Loanstypically offer lower interest rates than credit cards, especially for borrowers with good credit. According to recent Federal Reserve data, the average interest rate for a 24-month personal loan is approximately 9.5%, while the average credit card APR exceeds 16%. This significant difference makes loans more cost-effective for larger, longer-term financing needs.

However, this comparison isn’t always straightforward. Credit cards often feature introductory 0% APR periods on purchases and balance transfers (typically lasting 12-21 months), which can temporarily make them cheaper than loans. Additionally, rewards credit cards effectively provide a discount on purchases when paid in full each month.

Loan Vs Credit Card Apply Decision: Credit Cardsgenerally carry higher ongoing interest rates but offer more flexibility in repayment. The true cost depends largely on usage behavior—those who pay their balance in full each month avoid interest entirely, while those carrying balances face compounding interest that can quickly escalate debt.

Repayment Structure and Discipline

Loan Vs Credit Card Apply Decision: The fixed repayment schedule ofpersonal loansprovides built-in discipline. Borrowers know exactly when they’ll be debt-free if they make all scheduled payments. This structure prevents the “debt trap” phenomenon common with revolving credit, where minimum payments barely cover interest charges.

Credit cards require greater financial discipline. The flexibility to pay only a small minimum each month can lead to prolonged debt repayment. According to a CreditCards.com analysis, making only minimum payments on a $5,000 credit card balance at 17% APR would take over 20 years to repay and cost more than $6,700 in interest.

Impact on Credit Score

Loan Vs Credit Card Apply Decision: Both products affect your credit score, but through different mechanisms:

Loan Vs Credit Card Apply Decision: Personal Loansinitially cause a small dip in your score due to the hard inquiry and new account. However, they can positively impact your credit mix (which accounts for 10% of your FICO score) and, with consistent on-time payments, establish a positive payment history (35% of your score). Once paid off, closed loan accounts remain on your credit report for up to 10 years, continuing to contribute to your credit history length.

Credit Cards influence your score through several factors:

- Keeping this below 30%—and ideally below 10%—is optimal.

- Payment History (35%): Like loans, timely payments are crucial.

- Length of Credit History (15%): Older cards contribute positively to this factor.

- New Credit (10%): Opening several cards in a short period can temporarily lower your score.

Loan Vs Credit Card Apply Decision: Responsible credit card use—keeping balances low and paying on time—can build credit more quickly than installment loans in some cases, particularly through the utilization component.

Flexibility and Accessibility

Loan Vs Credit Card Apply Decision: Credit cardsoffer superior flexibility. You can use them for virtually any purchase, borrow only what you need when you need it, and have continuous access to funds as you pay down balances. Many cards also provide additional benefits like travel insurance, extended warranties, and price protection.

Loan Vs Credit Card Apply Decision: Personal loansprovide less flexibility once disbursed. You receive a lump sum upfront and cannot typically borrow additional funds without applying for a new loan. Some lenders offer loan “top-ups,” but these usually require reassessment of your financial situation.

Fees and Hidden Costs

Loan Vs Credit Card Apply Decision: Personal loanfees may include:

- Origination fees (1-8% of loan amount)

- Late payment fees

- Prepayment penalties (less common now but still exist with some lenders)

- Check processing fees

Credit card fees may include:

- Annual fees (for premium rewards cards)

- Balance transfer fees (typically 3-5%)

- Cash advance fees (often 5% with higher interest rates)

- Foreign transaction fees (though many cards now waive these)

- Late payment and over-limit fees

Strategic Decision Framework: When to Choose Each Option

Loan Vs Credit Card Apply Decision: When a Personal Loan Is Preferable

- Loan Vs Credit Card Apply Decision: Debt Consolidation: If you have multiple high-interest debts (especially credit cards), consolidating them with a personal loan at a lower fixed rate can save thousands in interest and simplify repayment.

- Large, One-Time Expenses: For major predictable expenses like home renovations, medical procedures, or weddings where you know the exact cost upfront, a personal loan provides appropriate funding with predictable repayment.

- When Discipline Is a Concern: If you struggle with spending discipline or tend to carry balances, the structured repayment of a loan prevents the revolving debt cycle.

- Loan Vs Credit Card Apply Decision: Lower Interest Needs: For borrowers with good credit who need to finance a purchase over time, personal loans generally offer lower rates than credit cards for terms beyond introductory periods.

- Fixed Budgeting Preference: Individuals who prefer consistent monthly payments for easier budgeting benefit from loan structures.

When a Credit Card Is Preferable

- Loan Vs Credit Card Apply Decision: Everyday Spending and Rewards: For regular purchases that you can pay off monthly, credit cards offer convenience, protection, and valuable rewards without interest costs.

- Short-Term Financing with 0% APR Offers: For planned purchases you can repay within an introductory 0% period, credit cards provide interest-free financing.

- Emergency Funding Without Predetermined Amounts: When you need access to funds but don’t know exactly how much, a credit line provides flexibility.

- Building Credit History: Responsible use of a credit card (keeping utilization low, paying on time) can effectively build or rebuild credit.

- Travel and Purchase Protections: For significant purchases or travel, credit card protections like extended warranties, rental car insurance, and fraud liability limits provide valuable security.

Hybrid Approaches

In some situations, a combination of both products might be optimal:

- Loan Vs Credit Card Apply Decision:

- Taking a personal loan for a major expense while using a credit card for daily purchases to earn rewards (paid in full monthly).

- Using a credit card for immediate emergency expenses while applying for a personal loan to pay off the balance if repayment will extend beyond a few months.

Case Studies: Real-World Applications

Case Study 1: Debt Consolidation

Loan Vs Credit Card Apply Decision: Situation: Maria has $15,000 in credit card debt across three cards with APRs ranging from 19-24%. She’s paying $450 monthly but making little progress on the principal.

Loan Solution: A 3-year personal loan at 10% APR would require $484 monthly payments, saving approximately $4,200 in interest compared to minimum credit card payments and paying off the debt in a fixed period.

Loan Vs Credit Card Apply Decision: Credit Card Solution: A balance transfer to a card with 0% APR for 18 months and a 3% transfer fee would cost $450 in fees. If Maria could pay $833 monthly during the promotional period, she could eliminate the debt interest-free.

Verdict: If Maria can maintain the higher payment during the promotional period, the balance transfer card saves more money. If not, the personal loan provides structured discipline with still-significant savings.

Case Study 2: Home Renovation

Loan Vs Credit Card Apply Decision: Situation: James needs $25,000 for a kitchen renovation with a 4-month timeline for contractors to complete the work.

Loan Solution: A 5-year personal loan at 8% APR would provide all funds upfront with predictable $507 monthly payments.

Credit Card Solution: A card with a 0% introductory period on purchases for 15 months would allow interest-free financing if James can repay approximately $1,667 monthly.

Loan Vs Credit Card Apply Decision: Verdict: If James has the cash flow to support the higher payment, the credit card option saves interest. If he prefers lower monthly payments, the personal loan is more suitable despite higher long-term costs.

Case Study 3: Emergency Medical Expense

Situation: Lisa faces an unexpected $8,000 medical bill with no emergency savings.

Loan Solution: A 3-year personal loan at 12% APR would create fixed monthly payments of $266.

Loan Vs Credit Card Apply Decision: Credit Card Solution: Putting the expense on a card with 16% APR would require minimum payments starting around $160 but extending repayment indefinitely if only minimums are paid.

Verdict: Given the unpredictability of Lisa’s financial recovery, the personal loan provides structured repayment that ensures the debt will be paid in a reasonable timeframe, likely making it the better choice despite potentially higher initial payments.

Future Considerations and Evolving Landscape

Loan Vs Credit Card Apply Decision: The financial landscape continues to evolve, with several trends impacting the loan vs. credit card decision:

- Digital Lending Platforms: Online lenders now offer faster personal loan approvals with more flexible criteria, making loans more accessible for various credit profiles.

- Specialized Credit Products: Industry-specific financing options (like medical credit cards with deferred interest) create new alternatives that blur traditional boundaries.

- Financial Technology Integration: Apps that help optimize debt repayment across multiple products are changing how consumers manage hybrid approaches.

- Regulatory Changes: Evolving regulations around lending practices, fee structures, and transparency continue to reshape both markets.

- Economic Factors: Interest rate environments, inflation, and economic conditions influence the relative attractiveness of fixed versus variable rate products.

Conclusion

The decision between a personal loan and a credit card depends fundamentally on your specific financial situation, discipline, and goals. Personal loans generally offer better value for large, predictable expenses requiring longer repayment periods, especially for debt consolidation. Credit cards provide superior flexibility for everyday spending, short-term financing needs, and those who can pay balances in full monthly.

Before deciding, consider these key questions:

- What is the exact amount needed?

- How long will I need to repay this debt?

- What is my credit profile and what rates am I likely to qualify for?

- How disciplined am I with repayment?

- Are there specific benefits (like rewards or protections) that sway the decision?

Ultimately, the “right” choice aligns with both your immediate financial need and your long-term financial health strategy. By understanding the mechanics, costs, and implications of each option, you can select the tool that not only addresses your current situation but supports your broader financial wellbeing.

Frequently Asked Questions

1. Which is easier to get approved for: a personal loan or a credit card?

Approval difficulty depends on your credit profile and the specific product. Generally, entry-level credit cards (particularly secured cards) are more accessible to those with poor or limited credit. Personal loans typically require fair to good credit (FICO scores of 580+) for unsecured options, though secured personal loans exist for those with lower scores. For premium products with the best rates and terms, both require good to excellent credit (scores of 670+).

3. What happens if I miss payments on either option?

For both personal loans and credit cards, missed payments typically trigger late fees and negative reporting to credit bureaus after 30 days, damaging your credit score. With credit cards, missed payments may also cause your APR to increase through penalty rates. With personal loans, consistent missed payments could lead to default and potentially legal action or debt collection. Both options offer hardship programs in some cases—contact your lender immediately if you anticipate payment difficulties.

4. Are there tax differences between personal loans and credit card debt?

Generally, neither personal loan interest nor credit card interest is tax-deductible for personal expenses. However, there are exceptions: interest on debt used for business purposes, investment property, or qualified educational expenses may be deductible in some circumstances. Additionally, if you use a personal loan for qualifying home improvements, the interest might be deductible (consult a tax professional for your specific situation).

5. How do balance transfer credit cards compare to debt consolidation loans?

Balance transfer cards with 0% introductory periods (typically 12-21 months) can be more cost-effective if you can pay off the entire balance during the promotional period, despite typical 3-5% balance transfer fees. Personal loans generally offer lower ongoing rates than credit cards after introductory periods expire and provide structured repayment timelines. The better option depends on: the total debt amount, how quickly you can repay it, your discipline with payments, and the specific terms you qualify for.