Post Office Saving Schemes Interest Rate 2026: पोस्ट ऑफिस की नई ब्याज दरें मार्च 2026; जानें किस स्कीम में मिलेगा सबसे ज्यादा मुनाफा और टैक्स छूट!

Introduction:

Post Office Saving Schemes Interest Rate 2026: साल 2026 में सुरक्षित निवेश (Safe Investment) के लिए पोस्ट ऑफिस की बचत योजनाएं एक बार फिर से निवेशकों की पहली पसंद बनी हुई हैं। भारत सरकार ने जनवरी-मार्च 2026 की तिमाही के लिए लघु बचत योजनाओं (Small Savings Schemes) के ब्याज दरों की घोषणा कर दी है। यदि आप शेयर बाजार के जोखिम से बचना चाहते हैं और सरकारी गारंटी के साथ अच्छा रिटर्न पाना चाहते हैं, तो “Post Office Saving Schemes Interest Rate 2026” की यह अपडेट आपके लिए बहुत महत्वपूर्ण है।

इस लेख में हम आपको पोस्ट ऑफिस की सभी प्रमुख योजनाओं जैसे पीपीएफ (PPF), सुकन्या समृद्धि (SSY), और सीनियर सिटीजन सेविंग्स स्कीम (SCSS) के ताजा ब्याज दरों और उनके फायदों के बारे में विस्तार से बताएंगे।

1. पोस्ट ऑफिस ब्याज दरें 2026 (Latest Interest Rate Table)

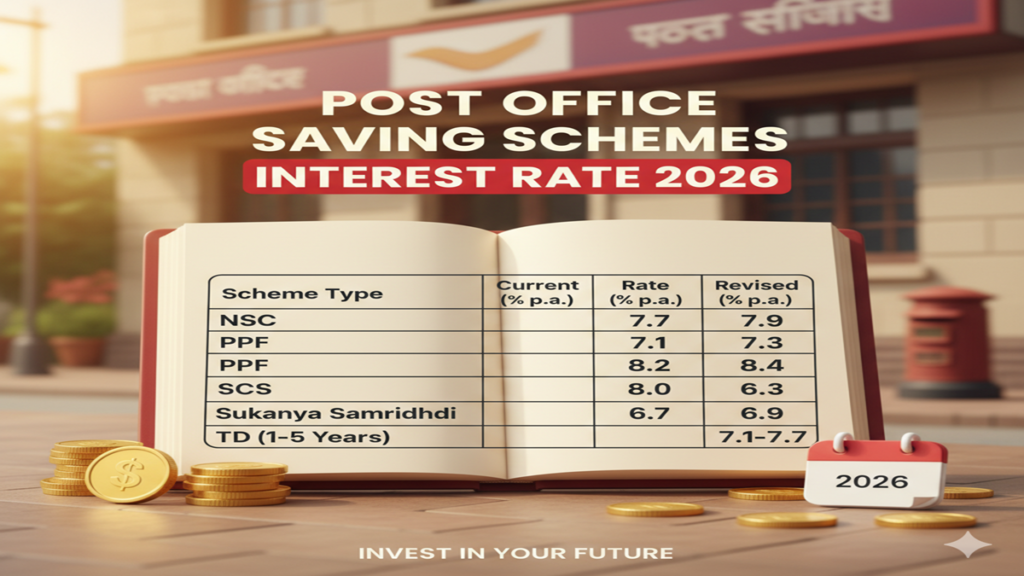

Post Office Saving Schemes Interest Rate 2026: वित्त मंत्रालय के नोटिफिकेशन के अनुसार, मार्च 2026 तिमाही के लिए ब्याज दरें इस प्रकार हैं:

| योजना का नाम (Scheme Name) | ब्याज दर (Interest Rate 2026)* |

| Savings Account | 4.0% |

| 1 Year Time Deposit (FD) | 6.9% |

| 2 Year Time Deposit (FD) | 7.0% |

| 3 Year Time Deposit (FD) | 7.1% |

| 5 Year Time Deposit (FD) | 7.5% |

| 5-Year Recurring Deposit (RD) | 6.7% |

| Senior Citizen Savings Scheme (SCSS) | 8.2% |

| Monthly Income Scheme (MIS) | 7.4% |

| National Savings Certificate (NSC) | 7.7% |

| Public Provident Fund (PPF) | 7.1% |

| Kisan Vikas Patra (KVP) | 7.5% (115 महीने में डबल) |

| Sukanya Samriddhi Account (SSA) | 8.2% |

*नोट: ये दरें 1 जनवरी 2026 से 31 मार्च 2026 तक प्रभावी हैं।

2. टॉप परफॉर्मिंग स्कीम्स का विश्लेषण (Detailed Analysis)

A. सुकन्या समृद्धि योजना (SSY):

Post Office Saving Schemes Interest Rate 2026: बेटियों के भविष्य के लिए यह सबसे लोकप्रिय योजना है। 8.2% के उच्च ब्याज दर के साथ, यह न केवल बेहतर रिटर्न देती है, बल्कि आयकर की धारा 80C के तहत टैक्स छूट भी प्रदान करती है।

B. सीनियर सिटीजन सेविंग्स स्कीम (SCSS):

Post Office Saving Schemes Interest Rate 2026: वरिष्ठ नागरिकों के लिए 8.2% की दर सबसे आकर्षक है। इसमें अधिकतम ₹30 लाख तक का निवेश किया जा सकता है, और ब्याज का भुगतान त्रैमासिक (Quarterly) किया जाता है।

C. मंथली इनकम स्कीम (MIS):

Post Office Saving Schemes Interest Rate 2026: यदि आप एकमुश्त पैसा जमा करके हर महीने पेंशन जैसी कमाई चाहते हैं, तो 7.4% की दर वाली MIS स्कीम बेहतरीन है। इसमें सिंगल अकाउंट में ₹9 लाख और जॉइंट अकाउंट में ₹15 लाख तक निवेश संभव है।

3. पोस्ट ऑफिस में निवेश के मुख्य फायदे (Benefits of Post Office Saving Schemes)

- संपूर्ण सुरक्षा (Sovereign Guarantee): चूंकि यह भारत सरकार द्वारा संचालित है, इसलिए आपका पैसा 100% सुरक्षित है।

- टैक्स सेविंग (Tax Benefits): NSC, PPF, और 5-साल की FD जैसी योजनाओं में निवेश करने पर इनकम टैक्स में छूट मिलती है।

- आसान पहुंच: भारत के किसी भी कोने में स्थित पोस्ट ऑफिस में आप खाता खुलवा सकते हैं। अब ‘IPPB’ ऐप के जरिए आप घर बैठे भी डिजिटल लेनदेन कर सकते हैं।

- न्यूनतम निवेश: कई योजनाएं मात्र ₹100 या ₹500 से शुरू की जा सकती हैं, जो छोटे बचतकर्ताओं के लिए वरदान हैं।

4. 2026 में निवेश की रणनीति (Investment Strategy)

- लॉन्ग टर्म: यदि आपका लक्ष्य 15 साल का है, तो PPF सबसे अच्छा है क्योंकि इसका ब्याज पूरी तरह टैक्स-फ्री होता है।

- शॉर्ट टर्म: 1 से 3 साल के लिए Time Deposit (FD) एक सुरक्षित विकल्प है।

- रेगुलर इनकम: रिटायर्ड लोगों के लिए SCSS और MIS का कॉम्बिनेशन सबसे सफल रहता है।

4. अक्सर पूछे जाने वाले प्रश्न (FAQs)

Q1: क्या पोस्ट ऑफिस के ब्याज दरें हर महीने बदलती हैं?

Ans: नहीं, भारत सरकार हर तीन महीने (Quarterly) में दरों की समीक्षा करती है और जरूरत पड़ने पर बदलाव करती है।

Q2: क्या मैं सुकन्या समृद्धि खाते को ऑनलाइन मैनेज कर सकता हूँ?

Ans: हाँ, यदि आपका खाता कोर बैंकिंग सॉल्यूशन (CBS) पोस्ट ऑफिस में है, तो आप इंटरनेट बैंकिंग या IPPB ऐप के जरिए पैसे जमा कर सकते हैं।

Q3: KVP में पैसा कितने समय में डबल होगा?

Ans: 2026 की दरों के अनुसार, किसान विकास पत्र (KVP) में आपका पैसा 115 महीनों (9 साल और 7 महीने) में दोगुना हो जाएगा।

Conclusion: सुरक्षित भविष्य की ओर कदम!

Post Office Saving Schemes Interest Rate 2026 की यह जानकारी आपको अपने वित्तीय लक्ष्यों को प्राप्त करने में मदद करेगी। बढ़ती महंगाई के दौर में सरकारी गारंटी वाला 7.5% से 8.2% का रिटर्न एक शानदार सौदा है। निवेश करने से पहले अपनी जरूरतों और टैक्स प्लानिंग को ध्यान में रखें और आज ही अपने नजदीकी डाकघर का दौरा करें।

Navigating Your Nest Egg: A Complete Guide to Post Office Saving Schemes Interest Rates in 2026

Post Office Saving Schemes Interest Rate 2026 In an era of volatile markets and complex financial instruments, the humble Post Office Saving Schemes (POSS) remain a bedrock of safety, predictability, and financial inclusion for millions of Indians. As we look ahead to 2026, understanding the trajectory of these interest rates is crucial for prudent financial planning, especially for risk-averse investors, retirees, and those building a balanced portfolio.

This article will delve into the expected interest rate landscape for Post Office schemes in 2026, analyze the governing factors, compare schemes, and provide strategic advice for investors.

The Bedrock: How Are Post Office Interest Rates Determined?

Post Office Saving Schemes Interest Rate 2026: Unlike bank fixed deposits, whose rates are largely determined by individual banks based on liquidity and competition, Post Office Saving Schemes have their interest rates set by the Government of India, specifically the Ministry of Finance, on a quarterly basis. Historically, however, these rates have been reviewed and announced for the entire financial year (April-March).

The primary benchmark for these rates is the yields on Government Securities (G-Secs) of comparable maturity. The government aims to keep POSS rates competitive with, and often slightly higher than, those offered by banks for similar tenors. This policy serves a dual purpose: it provides a safe return to savers and helps channel domestic savings into the government’s funding apparatus.

Post Office Saving Schemes Interest Rate 2026: For 2026, the direction of these rates will be intrinsically linked to the broader macroeconomic posture of the Reserve Bank of India (RBI). If inflation remains a concern and the RBI maintains a “higher for longer” repo rate regime into 2025, POSS rates for 2026 could see stability or even a marginal uptick in some schemes. Conversely, a significant economic slowdown prompting rate cuts could lead to a downward revision.

Projected Interest Rates for Post Office Schemes in 2026 (Forecast)

Post Office Saving Schemes Interest Rate 2026: While the official rates for the financial year 2026-27 will be announced in March 2026, we can make an educated forecast based on current trends and economic projections. The table below provides current rates (Q2 2024) and a projected range for 2026.

| Scheme Name | Current Interest Rate (2024-25) | Tenure | Projected Interest Rate Range for 2026-27 | Key Features for 2026 |

|---|---|---|---|---|

| Post Office Savings Account | 4.0% p.a. | – | 3.75% – 4.0% | Likely to remain stagnant. Minimal growth tool. |

| Post Office Time Deposit (POTD) | 1-Yr: 6.9%, 2-Yr: 7.0%, 3-Yr: 7.1%, 5-Yr: 7.5% | 1-5 Years | 6.75% – 7.75% | Rates may see marginal adjustment based on G-Sec yields. 5-Yr POTD remains a safe bet. |

| Post Office Recurring Deposit (RD) | 6.7% p.a. (Quarterly compounded) | 5 Years | 6.5% – 7.2% | Stable, disciplined saving tool. Rate likely to shadow 5-Yr G-Sec. |

| Post Office Monthly Income Scheme (POMIS) | 7.4% p.a. | 5 Years | 7.0% – 7.6% | Maximum investment limit doubled to ₹9 Lakh (Single) & ₹15 Lakh (Joint) in 2024. This makes it a cornerstone for retirees in 2026. |

| Post Office Senior Citizens Savings Scheme (SCSS) | 8.2% p.a. (Paid Quarterly) | 5 Years (extendable) | 8.0% – 8.5% | The flagship for retirees. Rate is mandated to be 100-150 bps above 5-Yr G-Sec. Most sensitive to RBI’s policy. |

| Public Provident Fund (PPF) | 7.1% p.a. (Compounded Annually) | 15 Years | 7.0% – 7.3% | Rate is less volatile. EEE tax status makes effective return much higher. |

| Kisan Vikas Patra (KVP) | 7.5% p.a. (Money doubles in ~115 months) | ~115 Months | 7.25% – 7.75% | Liquidity before maturity comes with penalties. Rate linked to medium-term G-Secs. |

| Sukanya Samriddhi Account (SSA) | 8.2% p.a. (Compounded Annually) | 21 Years | 8.0% – 8.4% | Likely to remain the highest-yielding POSS due to social incentive. EEE tax benefit. |

| National Savings Certificate (NSC) | 7.7% p.a. (Compounded Annually) | 5 Years | 7.5% – 8.0% | Popular for 5-year goal setting. Interest reinvested qualifies for 80C deduction. |

Post Office Saving Schemes Interest Rate 2026: Important Note: These are projections, not guarantees. Investors must verify rates from www.indiapost.gov.in when making decisions in 2026.

Comparative Analysis: Which Scheme Stands Out in 2026?

- For the Retiree (Primary Goal: Stable Monthly Income):

- Post Office Saving Schemes Interest Rate 2026: Top Contender: Post Office Monthly Income Scheme (POMIS). With the enhanced limit of ₹9 lakh, a single investor can potentially generate a steady ₹5,550 per month (at 7.4%). For joint holders (₹15 Lakh limit), this can be ₹9,250 per month. This, coupled with SCSS, forms a powerful income-generating portfolio.

- For the Long-Term Wealth Builder (Goal: Child’s Education/Marriage):

- Post Office Saving Schemes Interest Rate 2026: Top Contender: Sukanya Samriddhi Account (SSA). If the projection holds, its ~8.2% rate with EEE status is unbeatable for parents of a girl child. For others, the PPF remains the gold standard for its tax-free, long-term compounding.

- For the Conservative Saver (Goal: Capital Preservation & Beat Inflation):

- Top Contender: 5-Year Time Deposit (POTD) & NSC. These schemes are expected to offer rates (~7.5%) that may potentially outpace inflation, especially if it moderates to the RBI’s 4% target. They offer fixed returns with sovereign guarantee.

- For Tax Planning (Goal: Save Tax under 80C):

- Post Office Saving Schemes Interest Rate 2026: Top Contenders: PPF, SCSS, NSC, SSA, 5-Yr POTD. All these schemes qualify for deduction under Section 80C. The choice depends on liquidity needs and tenure. PPF and SSA offer the added benefit of tax-free maturity proceeds.

Strategic Considerations for Investing in 2026

- Post Office Saving Schemes Interest Rate 2026: Lock-in vs. Liquidity: Schemes like PPF and SSA have long lock-ins. SCSS allows premature withdrawal with a penalty. POTDs allow closure after 6 months with a reduced rate. Align the scheme’s liquidity with your future cash flow needs.

- Interest Payout Frequency: Need regular income? Choose SCSS (quarterly) or POMIS (monthly). For compounding magic, choose PPF, SSA, or NSC where interest is reinvested.

- The Tax Triangle (EEE vs. TTE): Understand the tax on interest. PPF, SSA are EEE (Exempt-Exempt-Exempt). SCSS & MIS interest is taxable but TDS applies only on SCSS if interest > ₹50,000/year. POTD interest is fully taxable and TDS applies if > ₹40,000/year.

- Post Office Saving Schemes Interest Rate 2026: The Digital Shift: The India Post Offices have aggressively promoted

DOP DigiBankand other online services. By 2026, expect even more seamless online account opening and management for most schemes, though in-person operation will remain vital for rural areas.

Challenges and the Road Ahead for 2026

- Post Office Saving Schemes Interest Rate 2026: Real Returns vs. Inflation: The perennial challenge. If inflation spikes beyond 6%, even the best POSS rates (~8%) offer a real return of only ~2%. Investors must consider allocating a portion to other asset classes.

- Post Office Saving Schemes Interest Rate 2026: Competition from Banks: With banks offering upwards of 7.5% on senior citizen FDs and special retail deposits, the competition for savings will intensify. The Post Office’s edge remains its sovereign guarantee and social trust.

- Post Office Saving Schemes Interest Rate 2026: Operational Delays: While improving, some post offices still face procedural delays. The digital push is key to mitigating this.

Conclusion: The Unwavering Pillar in Your 2026 Financial Plan

Post Office Saving Schemes Interest Rate 2026: As we project into 2026, Post Office Saving Schemes will continue to be a non-negotiable component of India’s savings landscape. They are not just financial instruments but vehicles of financial security for a vast populace. For the savvy investor, the key will be to mix and match these schemes based on individual goals—using SCSS/POMIS for income, PPF/SSA for long-term tax-free wealth, and POTDs/NSC for medium-term goals.

Post Office Saving Schemes Interest Rate 2026: While rates may fluctuate within a narrow band, the core virtues of safety, predictability, and accessibility will remain constant. Stay informed by checking official notifications in March 2026, consult with a financial advisor to align choices with your overall portfolio, and let Post Office Schemes provide the stable foundation upon which you can build a more ambitious, yet secure, financial future.

Frequently Asked Questions (FAQ) – Post Office Saving Schemes 2026

Q1: When will the Government officially announce the Post Office interest rates for 2026-27?

Post Office Saving Schemes Interest Rate 2026: A: The Government of India typically announces the interest rates for Post Office Saving Schemes for the upcoming financial year in the last week of March. The rates for the financial year 2026-27 (April 1, 2026, to March 31, 2027) will, therefore, be officially notified around March 2026. These will be published on the India Post website and through official gazettes.

Q2: If I open a 5-year Post Office Time Deposit (POTD) in 2025 at 7.5%, will my rate change in 2026?

Post Office Saving Schemes Interest Rate 2026: A: No, your rate will not change. One of the most attractive features of fixed-tenure Post Office schemes like POTD, SCSS, and NSC is that the interest rate is fixed for the entire tenure at the time of deposit. Your 7.5% rate will be locked in and protected from any potential rate cuts in 2026 or beyond until maturity. This “lock-in” feature is a significant advantage during a potential falling interest rate cycle.

Q3: Which scheme is likely to offer the highest interest rate in 2026, and is it taxable?

Post Office Saving Schemes Interest Rate 2026: A: Based on current and projected trends, the Sukanya Samriddhi Account (SSA) and the Senior Citizens Savings Scheme (SCSS) are expected to vie for the highest nominal rate, potentially in the 8.0% – 8.5% range.

SSA Interest: It is completely tax-free (EEE category). The interest earned, the principal invested (under 80C), and the maturity amount are all exempt from tax.

SCSS Interest: It is fully taxable and added to your income as per your slab rate. Furthermore, Tax Deducted at Source (TDS) is applicable if the interest income from SCSS exceeds ₹50,000 in a financial year.

Q4: With the increased limit, is the Monthly Income Scheme (POMIS) a better option than a Senior Citizen FD from a bank in 2026?

Post Office Saving Schemes Interest Rate 2026: A: It depends on your priority:

Choose POMIS if: Sovereign guarantee and stable, predictable monthly income are your primary concerns. The rate is fixed for 5 years, and the backing of the Government of India provides unparalleled safety.

Choose a Bank Senior Citizen FD if: You are chasing a slightly higher interest rate (banks often offer 25-50 bps more for seniors) or need more flexibility with tenure (from 7 days to 10 years). Bank FDs may also offer easier premature withdrawal options, albeit with penalties.

For most retirees seeking peace of mind, a combination of both (POMIS for core income and an FD for liquidity) is an optimal strategy for 2026.

Q5: Can I manage and operate all my Post Office accounts online in 2026?

Post Office Saving Schemes Interest Rate 2026: A: The Department of Posts has been rapidly expanding its digital capabilities. By 2026, it is highly likely that a majority of savings and certificate schemes will be accessible for online management through the DOP DigiBank app and the India Post website. This includes balance inquiries, viewing passbooks, downloading statements, and even initiating some transactions. However, certain actions like first-time account opening, nomination changes, or premature closure of some certificates may still require an in-person visit to your home post office. The process is expected to be far more digitized, but not necessarily 100% paperless for all operations.