Personal Loan Tenure Explained: पर्सनल लोन की अवधि का आपके बजट और ब्याज पर क्या प्रभाव पड़ता है? पूरी जानकारी!

Introduction:

Personal Loan Tenure Explained जब भी हम पर्सनल लोन के लिए आवेदन करते हैं, तो बैंक हमसे दो मुख्य सवाल पूछता है—”कितना लोन चाहिए?” और “कितने समय के लिए चाहिए? आती है, लेकिन क्या यह वाकई सस्ता पड़ता है?

“Personal Loan Tenure Explained” के इस विस्तृत लेख में हम समझेंगे कि लोन की अवधि आपके वित्तीय बोझ को कैसे प्रभावित करती है और 2026 की ब्याज दरों के हिसाब से आपको सही चुनाव कैसे करना चाहिए।

1. पर्सनल लोन टेन्योर क्या है? (What is Tenure?)

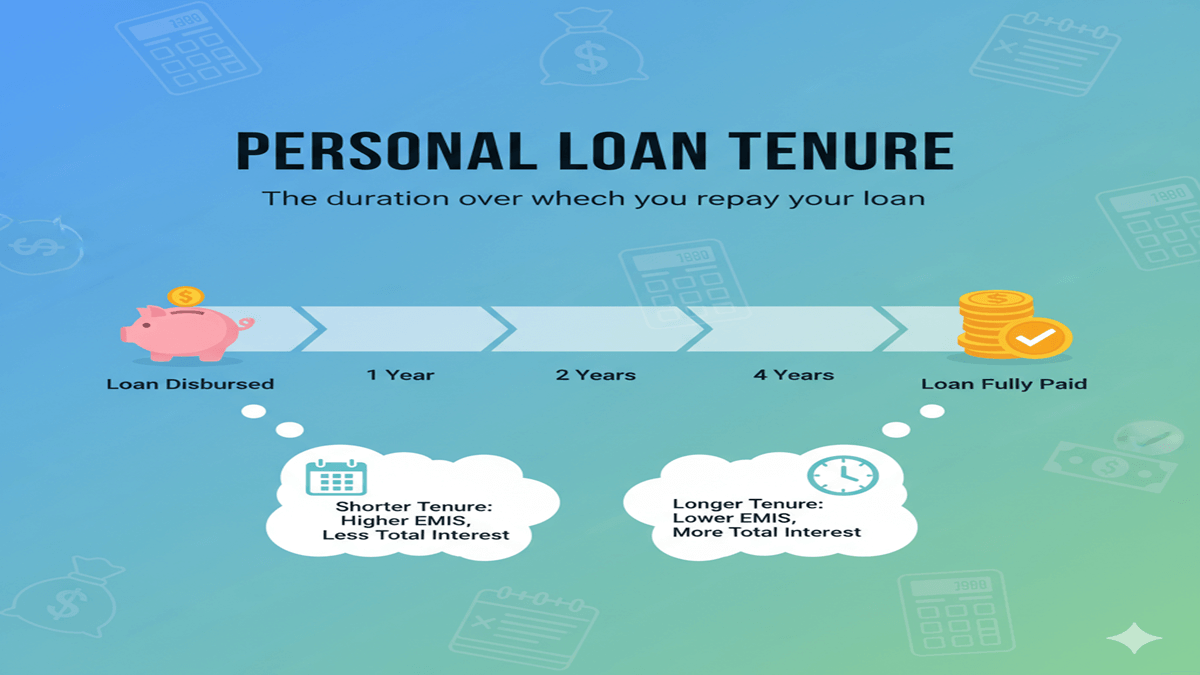

Personal Loan Tenure Explained पर्सनल लोन टेन्योर वह निश्चित समय सीमा है जिसके भीतर आपको उधार ली गई राशि और उस पर लगने वाले ब्याज को मासिक किस्तों (EMI) के रूप में वापस करना होता है। भारत में आमतौर पर पर्सनल लोन का टेन्योर 12 महीने (1 साल) से लेकर 60 महीने (5 साल) तक होता है। कुछ बैंक अब इसे 7 साल तक भी बढ़ा रहे हैं।

2. छोटी अवधि बनाम लंबी अवधि (Short-term vs Long-term)

Personal Loan Tenure Explained लोन की अवधि का सीधा संबंध आपके ब्याज (Interest) और ईएमआई (EMI) से होता है।

A. छोटी अवधि (Short Tenure: 1-2 साल):

- ईएमआई: इसमें आपकी हर महीने की किस्त (EMI) ज्यादा होती है।

- ब्याज: चूंकि आप लोन जल्दी चुका देते हैं, इसलिए आपको कुल ब्याज बहुत कम देना पड़ता है।

- किसके लिए सही है: जिनकी आय अधिक है और जो जल्द से जल्द कर्ज मुक्त होना चाहते हैं।

B. लंबी अवधि (Long Tenure: 4-5 साल):

- ईएमआई: हर महीने की किस्त काफी कम और जेब के लिए आसान होती है।

- ब्याज: लोन चुकाने में समय ज्यादा लगता है, जिससे बैंक आपसे बहुत अधिक ब्याज वसूलता है।

- किसके लिए सही है: जिनका मासिक बजट टाइट है और जो कम ईएमआई का बोझ उठाना चाहते हैं।

3. टेन्योर का ब्याज पर प्रभाव (Case Study 2026)

Personal Loan Tenure Explained मान लीजिए आपने ₹5,00,000 का लोन 12% ब्याज दर पर लिया है। आइए देखें समय के साथ गणित कैसे बदलता है:

| लोन अवधि (Tenure) | मासिक ईएमआई (EMI) | कुल देय ब्याज (Total Interest) |

| 2 साल | ₹23,537 | ₹64,882 |

| 3 साल | ₹16,607 | ₹97,852 |

| 5 साल | ₹11,122 | ₹1,67,333 |

निष्कर्ष: यदि आप 2 साल के बजाय 5 साल का टेन्योर चुनते हैं, तो आपकी ईएमआई तो आधी हो जाती है, लेकिन आपको ₹1 लाख से ज्यादा का अतिरिक्त ब्याज देना पड़ता है।

4. सही टेन्योर चुनने के लिए 3 टिप्स (Smart Tips)

- अपनी चुकौती क्षमता (Repayment Capacity) देखें: अपनी सैलरी में से अन्य खर्चों को निकालकर देखें कि आप कितनी अधिकतम ईएमआई दे सकते हैं। ईएमआई आपकी नेट इनकम के 30-40% से ज्यादा नहीं होनी चाहिए।

- प्री-पेमेंट चार्ज चेक करें: यदि आप भविष्य में बोनस मिलने पर लोन जल्दी बंद करना चाहते हैं, तो ऐसा बैंक चुनें जिसमें प्री-पेमेंट या फोरक्लोजर चार्ज कम या जीरो हो।

- ब्याज दर का प्रकार: फिक्स्ड रेट और फ्लोटिंग रेट को समझें। 2026 में यदि ब्याज दरें घटने की उम्मीद है, तो फ्लोटिंग रेट बेहतर हो सकता है।

4. अक्सर पूछे जाने वाले प्रश्न (FAQs)

Q1: क्या मैं पर्सनल लोन लेने के बाद उसका टेन्योर बदल सकता हूँ?

Ans: कुछ बैंक ‘Restructuring’ की अनुमति देते हैं, लेकिन इसके लिए आपको प्रोसेसिंग फीस देनी पड़ सकती है और यह बैंक की पॉलिसी पर निर्भर करता है।

Q2: क्या सबसे छोटा टेन्योर हमेशा सबसे अच्छा होता है?

Ans: वित्तीय रूप से हाँ, क्योंकि ब्याज बचता है। लेकिन यदि बहुत ज्यादा ईएमआई के कारण आप अन्य जरूरी खर्चे नहीं कर पा रहे हैं, तो मध्यम अवधि (3 साल) चुनना समझदारी है।

Q3: टेन्योर का क्रेडिट स्कोर पर क्या असर होता है?

Ans: टेन्योर लंबा हो या छोटा, यदि आप समय पर ईएमआई भरते हैं, तो आपका क्रेडिट स्कोर बेहतर होता है। हालांकि, बहुत लंबे समय तक कर्ज में रहना आपकी ‘Credit Hunger’ को दर्शा सकता है।

Conclusion: संतुलन बनाना जरूरी है!

Personal Loan Tenure Explained का मुख्य सार यह है कि आपको अपने मासिक बजट और कुल ब्याज के बीच एक संतुलन बनाना चाहिए। 2026 के महंगाई के दौर में, कोशिश करें कि लोन की अवधि उतनी ही रखें जितनी आपकी जेब गवाही दे, ताकि आप ब्याज के जाल में न फंसें।

Personal Loan Tenure Explained: Your Guide to Choosing the Right Repayment Timeline

Personal Loan Tenure Explained In the realm of personal finance, a personal loan stands as a versatile and accessible tool for bridging monetary gaps, funding aspirations, or consolidating pressing debts. However, the true power of this financial instrument lies not just in securing the loan amount, but in strategically tailoring its structure to your unique economic reality. At the heart of this customization is a single, critical decision: choosing your loan tenure.

Loan tenure—the predetermined period over which you agree to repay the borrowed sum plus interest—is far more than a mere timeline. It is the lever that directly controls your monthly financial burden, the total cost of your borrowing, and the long-term flexibility of your budget. Selecting the right tenure is a balancing act between immediate affordability and ultimate financial efficiency.

This comprehensive guide will navigate you through the intricacies of personal loan tenure, empowering you to make an informed choice that aligns with your goals and safeguards your financial health.

The Fundamental Mechanics: How Tenure Impacts Your Loan

Personal Loan Tenure Explained To understand tenure, one must first grasp its direct mathematical relationship with two key components of your loan: the Equated Monthly Installment (EMI) and the Total Interest Payable.

- EMI (Equated Monthly Installment): This is the fixed amount you pay to the lender every month until the loan is fully repaid. An EMI comprises two parts: a portion that goes toward repaying the principal amount borrowed, and a portion that covers the interest charged by the lender.

- Total Interest Payable: This is the cumulative sum of all interest components paid over the entire life of the loan.

The tenure acts as the pivot between these two elements, governed by a simple inverse relationship:

- Longer Tenure = Lower EMI, but Higher Total Interest.

- Spreading the principal over more months reduces the monthly outgo, making the loan seem more affordable on a cash-flow basis. However, since the principal remains outstanding for a longer period, interest accrues over more months, significantly increasing the total amount repaid to the lender.

- Compressing the repayment schedule increases the monthly financial commitment. Yet, the loan is settled faster, leaving less time for interest to accumulate, resulting in substantial interest savings and a lower overall cost of borrowing.

The Detailed Pros and Cons: Short vs. Long Tenure

Personal Loan Tenure Explained Choosing a tenure is not about finding a universally “correct” answer, but about identifying the best fit for your circumstances. Let’s dissect the advantages and disadvantages of each approach.

Opting for a Shorter Loan Tenure (e.g., 1-3 years)

Advantages:

- Personal Loan Tenure Explained Substantial Interest Savings: This is the most compelling benefit. You pay far less to the bank over the life of the loan. For example, on a ₹5 lakh loan at 12% p.a., choosing a 2-year tenure over a 5-year tenure can save you over ₹1 lakh in interest.

- Debt Freedom, Faster: You clear your liability quickly, freeing up your income and credit profile for other goals or emergencies much sooner.

- Improved Credit Discipline: The necessity of managing a higher EMI can instill strong financial discipline.

- Personal Loan Tenure Explained Often Attracts Lower Interest Rates: Some lenders offer marginally lower interest rates for shorter-tenure loans, as their money is at risk for a shorter period.

Disadvantages:

- High Monthly Outgo: The significantly larger EMI can strain your monthly budget, leaving less room for other expenses, investments, or discretionary spending.

- Reduced Cash Flow Flexibility: A large portion of your income is committed to the loan, reducing your ability to handle unexpected financial shocks.

- Potential for Default Risk: If your income is unstable, the high EMI increases the risk of missing payments, leading to penalties and credit score damage.

Personal Loan Tenure Explained Ideal For: Individuals with high, stable, and predictable income; those with large bonuses or variable pay that can be used for prepayment; borrowers who prioritize minimizing total cost over monthly cash flow; or for funding needs where the asset (like a vacation) doesn’t justify long-term debt.

Opting for a Longer Loan Tenure (e.g., 5-7 years)

Advantages:

- Highly Affordable EMI: The primary appeal. The monthly payment is manageable, easing immediate budget pressure and making larger loan amounts accessible.

- Enhanced Financial Breathing Room: The lower EMI frees up cash for other essential expenses, investments (which may yield returns higher than your loan interest), or building an emergency fund.

- Personal Loan Tenure Explained Easier Qualification: A lower EMI-to-income ratio makes it easier to meet a lender’s eligibility criteria, especially for those with moderate incomes.

Disadvantages:

- Significantly Higher Total Cost: You pay a premium for the convenience of a low EMI. The interest paid over the extended period can often be staggering, sometimes nearing or even exceeding the original principal.

- Longer Debt Trap: You remain in debt for an extended period, which can delay other financial milestones like saving for a home, retirement, or your child’s education.

- Personal Loan Tenure Explained More Susceptible to Interest Rate Changes: If you have a floating interest rate, a longer tenure exposes you to more cycles of potential rate hikes over time.

Ideal For: Borrowers with fixed or moderate incomes who need certainty in their monthly budgets; those using the loan for essential consolidation of high-interest debts (like credit cards); or for emergencies where the primary goal is immediate fund access with minimal monthly disruption.

The Golden Rule: The 35-40% EMI-to-Income Ratio

Personal Loan Tenure Explained Financial advisors universally recommend that your total EMI obligations (including the new personal loan) should not exceed 35-40% of your net monthly income (income after taxes). This is not just a guideline; it’s a critical guardrail for financial stability.

- How to Calculate: If your take-home pay is ₹80,000 per month, your total EMIs should ideally be capped at ₹28,000 – ₹32,000.

- Breaching this threshold is a red flag for potential default and severe financial stress.

- Personal Loan Tenure Explained Tenure’s Role: If a shorter tenure pushes your EMI above this safe zone, a longer tenure becomes a necessary tool to bring the EMI back within sustainable limits. Always use this ratio as a starting point for your tenure decision.

Strategic Considerations: Beyond Just Math

Personal Loan Tenure Explained The right tenure choice involves both quantitative calculation and qualitative life assessment.

- Your Life Stage & Future Goals:

- Young Professional (20s-30s): You might prioritize keeping EMIs low to allow for career flexibility, upskilling, or initial investments. A medium tenure could be a balance. However, starting with a disciplined shorter tenure can build great habits.

- Personal Loan Tenure Explained Established Professional with Family (30s-50s): You have multiple financial goals (child’s education, home purchase, retirement). A shorter personal loan tenure to clear debt quickly may be preferable to avoid clashing with these future liabilities.

- Pre-Retiree (50s+): The goal should be to enter retirement debt-free. A tenure that ends before your retirement date is absolutely non-negotiable.

- Income Stability & Growth Trajectory:

- Personal Loan Tenure Explained Salaried with Steady Increments: If you have high confidence in predictable salary growth, you could opt for a slightly higher EMI (shorter tenure) now, banking on future income increases to make it feel lighter.

- Variable Income or Self-Employed: A longer tenure with a comfortable EMI provides a crucial safety buffer during months of lower cash flow. The focus here is on sustainability over aggressive repayment.

- The Purpose of the Loan:

- Personal Loan Tenure Explained Debt Consolidation: The goal is to simplify and reduce cost. Choose a tenure that gives you an EMI lower than your combined previous payments, but aim for the shortest tenure you can afford to maximize interest savings on the consolidated amount.

- Medical Emergency: The need is urgent, and financial stress is high. A longer tenure to minimize monthly burden during recovery may be the most humane choice.

- Discretionary Spending (Wedding, Vacation): Since this funds a depreciating expense, a shorter tenure is strongly advised to avoid paying excessive interest for something with no lasting financial value.

The Power of Prepayment: Your Secret Weapon

Personal Loan Tenure Explained Most personal loans in India allow for prepayment or foreclosure, either partially or in full, often after a lock-in period (like 6-12 months). This feature can be strategically combined with tenure selection.

- Strategy: You could consciously choose a longer tenure to secure a low, manageable EMI, but aggressively prepay whenever you have surplus cash—from bonuses, tax refunds, or investment maturity.

- Benefit: This hybrid approach gives you the safety net of a low mandatory payment while allowing you to reduce the principal faster, thereby cutting down the total interest and effectively shortening the loan’s actual lifespan on your own terms.

- Personal Loan Tenure Explained Check Fine Print: Always verify prepayment charges (which are now heavily regulated but may still exist for fixed-rate loans) before adopting this strategy.

Navigating the Process: A Step-by-Step Guide

- Determine the Exact Loan Amount: Borrow only what you absolutely need, not the maximum you’re offered.

- Know Your Numbers: Calculate your precise net monthly income and existing EMI obligations.

- Use Online EMI Calculators: Every bank and financial website offers these tools. Input your desired loan amount, interest rate, and test different tenures (2, 3, 5, 7 years). Observe the dramatic change in both the EMI and the “Total Interest Paid” figures.

- Apply the 35% Rule: See which tenures keep your projected EMI within the safe limit of 35% of your income.

- Run a Future Budget Simulation: Don’t just look at today. Can you comfortably pay this EMI for the next 3, 5, or 7 years, considering potential life changes?

- Compare Lender Terms: Tenure options vary. Some lenders offer a maximum of 5 years, others 6 or 7. Choose a lender whose offered tenures align with your calculated sweet spot.

- Formalize and Commit: Once selected, ensure you have the discipline to stick to the repayment plan.

Conclusion: A Decision of Empowerment

Personal Loan Tenure Explained Selecting your personal loan tenure is a profound exercise in financial self-awareness. It forces you to confront your income stability, expenditure habits, future obligations, and ultimate goals. There is no trophy for choosing the shortest tenure if it leads to daily financial anxiety, just as there is no wisdom in a decades-long EMI that bleeds you dry in interest.

Personal Loan Tenure Explained The most prudent path often lies in a balanced, middle-ground tenure—one that results in an EMI comfortably within your safe repayment ratio, while not excessively inflating the total interest cost. Pair this with a proactive prepayment mindset, and you transform your loan from a passive debt into an actively managed financial tool.

Remember, the goal is not just to get a loan, but to get out of it stronger. By investing time in understanding and strategically choosing your tenure, you take a decisive step toward that very outcome.

Frequently Asked Questions (FAQs)

1. Can I change my loan tenure after the loan has been disbursed?

Personal Loan Tenure Explained Typically, the tenure is fixed at the time of sanction and cannot be directly altered during the loan term. However, you have two effective alternatives:

- Prepayment: Making a partial prepayment can often be coupled with a request to reduce the EMI (keeping the tenure same) or to reduce the tenure (keeping the EMI same). Lenders may allow this recalculation, sometimes for a fee.

- Loan Refinancing: You can apply to transfer your remaining loan balance to a new lender (or sometimes the same one) for a fresh loan with a different tenure that better suits your current needs. This is subject to credit approval and may involve charges.

2. Is a longer tenure always bad because of higher interest?

Personal Loan Tenure Explained Not necessarily “bad,” but it is “costlier.” The trade-off is affordability. A longer tenure can be a financially responsible choice if it is the only way to keep your EMI within a safe, sustainable percentage of your income (the 35-40% rule). It is better to pay more interest over time than to default on a high-EMI, short-tenure loan. The key is to be aware of the extra cost and consider prepayments later to mitigate it.

3. How does my credit score affect the tenure I am offered?

Personal Loan Tenure Explained Your credit score primarily influences the interest rate you are offered, not directly the tenure. A high credit score may help you secure a lower interest rate. However, this lower rate can expand your options—it might make a shorter tenure more affordable (as the EMI would be lower for the same period), or make a longer tenure less expensive in total interest. Lenders are generally more flexible with tenure offerings to borrowers with excellent credit profiles.

4. What happens if I miss an EMI during my loan tenure?

Personal Loan Tenure Explained Missing an EMI has serious consequences:

- Late Payment Fees: You will be charged a hefty penalty, which increases your total cost.

- Credit Score Damage: The missed payment will be reported to credit bureaus (CIBIL, etc.), causing a significant and long-lasting drop in your credit score.

- Increased Interest Cost: On some loans, default may lead to penalty interest rates.

- Legal Action: Persistent default can lead to recovery proceedings and legal action from the lender.

If you anticipate difficulty, immediately contact your lender to discuss a possible solution, such as a temporary EMI holiday (if offered), rather than simply missing a payment.

5. Should I choose the maximum tenure offered to get the lowest possible EMI?

Personal Loan Tenure Explained This is generally not advisable. While it minimizes your monthly commitment, it maximizes the total interest paid, often to an extreme degree. You should view the maximum tenure as the outer boundary of your options, not the default choice. Use an EMI calculator to find the shortest tenure that still results in an EMI you can manage without stress. Start your evaluation from a 3-4 year tenure and increase it only if the EMI is unmanageable, rather than starting at the 7-year maximum and working down.