Bajaj Finserv EMI Card Charges Details: क्या आपका बजाज कार्ड महंगा पड़ रहा है? जानें हर एक चार्ज की पूरी सच्चाई!

Introduction:

Bajaj Finserv EMI Card Charges Details: आजकल खरीदारी करना बहुत आसान हो गया है, खासकर Bajaj Finserv EMI Card की वजह से। यह कार्ड आपको इलेक्ट्रॉनिक्स, मोबाइल और घरेलू सामानों को ‘No Cost EMI’ पर खरीदने की सुविधा देता है। लेकिन, क्या आपने कभी सोचा है कि जिस कार्ड को हम ‘फ्री’ या ‘सस्ता’ समझते हैं, उसके पीछे कितने प्रकार के शुल्क (Charges) छिपे होते हैं?

यदि आप “Bajaj Finserv EMI Card Charges Details” ढूंढ रहे हैं, तो यह लेख आपके लिए बहुत महत्वपूर्ण है। कार्ड के जॉइनिंग शुल्क से लेकर ईएमआई बाउंस होने तक के सभी खर्चों को समझना आपके वित्तीय स्वास्थ्य के लिए जरूरी है।

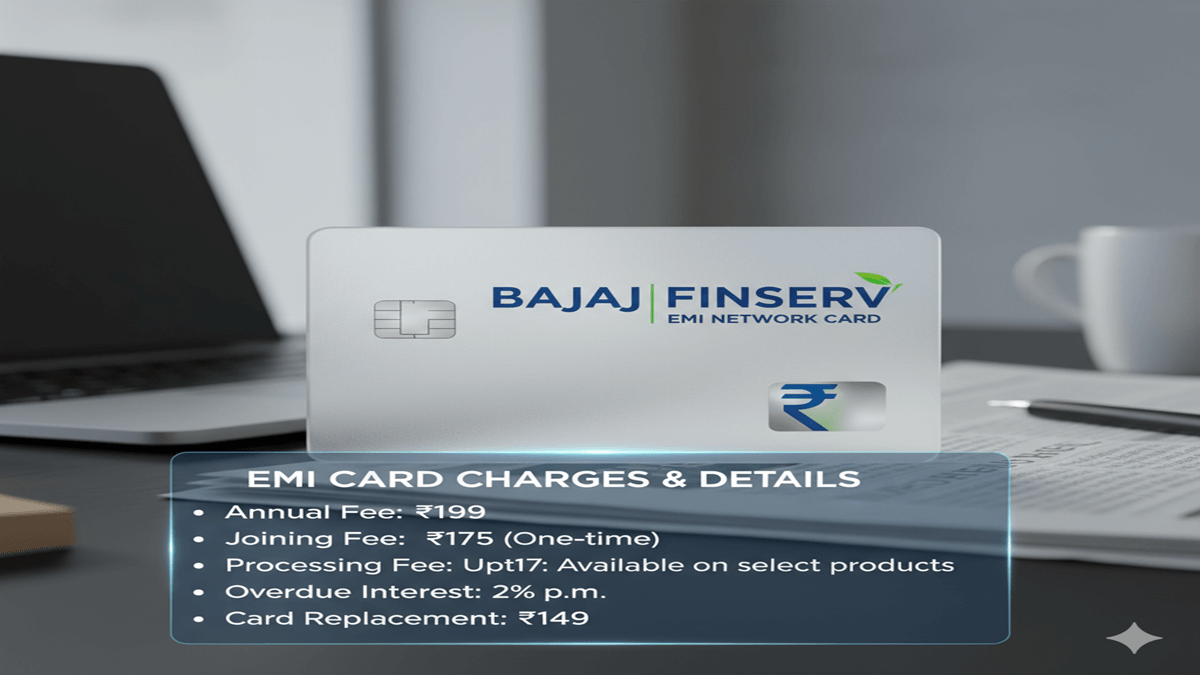

1. कार्ड जॉइनिंग और एनुअल फीस (Joining & Annual Charges)

Bajaj Finserv EMI Card Charges Details: जब आप बजाज ईएमआई कार्ड के लिए आवेदन करते हैं, तो आपको कुछ शुरुआती शुल्क देने होते हैं:

- Insta EMI Card Joining Fee: वर्तमान में यह शुल्क लगभग ₹530 से ₹599 (GST सहित) के बीच होता है। यह केवल एक बार देना होता है।

- Annual Maintenance Charge (AMC): यदि आपने पूरे साल में कार्ड का उपयोग करके कोई खरीदारी नहीं की है, तो आपसे लगभग ₹117 का वार्षिक शुल्क लिया जाता है। (नोट: यदि कार्ड सक्रिय रूप से उपयोग हो रहा है, तो कई बार यह माफ कर दिया जाता है)।

2. ट्रांजैक्शन और प्रोसेसिंग फीस (Transaction Fees)

Bajaj Finserv EMI Card Charges Details: कार्ड का उपयोग करते समय लगने वाले मुख्य शुल्क इस प्रकार हैं:

- Processing Fee: हर बार जब आप कोई सामान खरीदते हैं, तो बजाज आपसे एक छोटी प्रोसेसिंग फीस लेता है। यह आमतौर पर ₹49 से ₹199 के बीच होती है।

- Network Fee: यह एक ऐसा शुल्क है जो अक्सर लोगों की नजर से बच जाता है। हर नई खरीदारी पर आपसे ₹49 से ₹69 की नेटवर्क फीस ली जा सकती है।

3. पेनाल्टी और बाउंस चार्जेज (Penalty & Bounce Charges)

Bajaj Finserv EMI Card Charges Details: यह सबसे महत्वपूर्ण हिस्सा है, क्योंकि यहाँ आपको सबसे ज्यादा पैसा खर्च करना पड़ सकता है:

- EMI Bounce Charges: अगर आपके बैंक खाते में पैसे नहीं हैं और ईएमआई बाउंस हो जाती है, तो बजाज फिनसर्व आपसे ₹450 से ₹500 प्रति बाउंस वसूलता है। इसके अलावा, आपका बैंक भी अलग से बाउंस चार्ज लेगा।

- Late Payment Penalty: ईएमआई की तारीख निकलने के बाद बकाया राशि पर 2% से 3% प्रति माह की दर से जुर्माना लगाया जा सकता है।

- Mandate Rejection Charges: यदि आपका ई-मैंडेट (E-Mandate) सफल नहीं होता है, तो ₹450 तक का शुल्क लग सकता है।

4. अन्य महत्वपूर्ण शुल्क (Other Charges Table)

| शुल्क का नाम | अनुमानित राशि (Approx) |

| Loan Foreclosure | आमतौर पर फ्री (कुछ मामलों में लागू) |

| Document Retention | ₹50 – ₹100 |

| Statement of Account | ऑनलाइन फ्री / फिजिकल कॉपी ₹50 |

| Card Replacement | ₹199 |

5. चार्जेज से कैसे बचें? (Tips to Avoid Extra Charges)

- समय पर भुगतान: हमेशा अपनी ईएमआई की तारीख (आमतौर पर हर महीने की 2 या 5 तारीख) से पहले खाते में पर्याप्त बैलेंस रखें।

- ऑनलाइन स्टेटमेंट: फिजिकल कॉपी मंगवाने के बजाय ‘Bajaj Finserv App’ का उपयोग करें, जो बिल्कुल मुफ्त है।

- ई-मैंडेट अपडेट: यदि आप अपना बैंक खाता बदलते हैं, तो उसे तुरंत अपडेट करें ताकि बाउंस चार्जेज से बचा जा सके।

4. अक्सर पूछे जाने वाले प्रश्न (FAQs)

Q1: क्या बजाज ईएमआई कार्ड पूरी तरह फ्री है?

Ans: नहीं, इसमें जॉइनिंग फीस और ट्रांजैक्शन के समय प्रोसेसिंग फीस लगती है। ‘No Cost EMI’ का मतलब है कि आपसे अतिरिक्त ब्याज नहीं लिया जाएगा, लेकिन अन्य शुल्क लागू रहेंगे।

Q2: ईएमआई बाउंस होने पर क्या मेरा सिबिल (CIBIL) स्कोर प्रभावित होगा?

Ans: हाँ, ईएमआई बाउंस होने से न केवल भारी शुल्क लगता है, बल्कि आपका सिबिल स्कोर भी गिर जाता है, जिससे भविष्य में लोन मिलना मुश्किल हो सकता है।

Q3: क्या मैं अपना कार्ड बंद करवा सकता हूँ?

Ans: हाँ, आप कस्टमर केयर को कॉल करके या नजदीकी शाखा में जाकर अपना कार्ड बंद करवा सकते हैं, बशर्ते आपके सभी बकाया (Dues) क्लियर हों।

Conclusion: सावधानी ही सुरक्षा है!

Bajaj Finserv EMI Card खरीदारी के लिए एक शानदार विकल्प है, बशर्ते आप इसके Charges Details को अच्छी तरह समझते हों। यदि आप समय पर भुगतान करते हैं, तो यह कार्ड आपके लिए वरदान है, लेकिन लापरवाही बरतने पर चार्जेज का बोझ भारी पड़ सकता है। हमेशा खरीदारी से पहले ‘Terms & Conditions’ को ध्यान से पढ़ें।

Demystifying Bajaj Finserv EMI Card Charges: A Complete Guide to Fees, Interest & Hidden Costs

Bajaj Finserv Emi Card Charges Details The Bajaj Finserv EMI Card is a powerful financial tool that has revolutionized how millions of Indians shop. It offers instant pre-approved credit at a vast network of over 1.5 million partner stores, both online and offline, allowing you to convert purchases into easy monthly installments (EMIs). However, the true cost of this convenience lies in understanding its fee structure.

Bajaj Finserv EMI Card Charges Details: While marketed as a “zero-cost EMI” product, certain transactions and usage patterns attract specific charges. This comprehensive guide, spanning 2000+ words, will break down every possible Bajaj Finserv EMI Card charge in detail, helping you use the card smartly and avoid unnecessary expenses. Think of this as your official manual to the card’s financial fine print.

Understanding the Card’s Core Function: It’s Not a Credit Card

Bajaj Finserv EMI Card Charges Details: First, a crucial distinction. The Bajaj Finserv EMI Card is not a traditional credit card. It is a line of credit (like a digital loan) primarily designed for converting purchases into EMIs at partner merchants. You cannot use it for arbitrary ATM withdrawals or general swipes at non-partner stores like a regular credit card. This focused design is key to understanding its charge structure.

Part 1: Standard Fees & Joining Charges

Bajaj Finserv EMI Card Charges Details: Contrary to popular belief, the Bajaj Finserv EMI Card itself does not have a universal joining or annual fee. It is often provided as a free benefit, especially when you have an existing relationship with Bajaj Finserv (like a loan). However, there are scenarios where fees apply:

- Joining/Membership Fee: This is typically ₹0. The card is usually offered as a pre-approved, free accessory to creditworthy customers. Always confirm this during the application process, as special promotional cards or variants could have a nominal fee (rare).

- Annual Renewal Fee: Similar to the joining fee, the standard annual renewal charge is ₹0. You are not billed yearly simply for holding the card.

Key Takeaway: The card’s primary access is free. The costs come into play based on how you use it.

Part 2: The Detailed Breakdown of Usage-Based Charges

Bajaj Finserv EMI Card Charges Details: This is the most important section. Charges are triggered by specific actions and transaction types.

1. Finance Charges (Interest on EMIs)

This is the core cost of availing credit.

- Standard EMI Purchases: When you buy a product on EMI at a partner store, an interest rate is applied. This rate varies based on the product category, merchant, promotional offer, and your credit profile. It can range from 12% to 24% per annum or more.

- “No-Cost EMI” Schemes: This is a marketing highlight. Here, the interest is borne by the brand or Bajaj Finserv as a promotion, NOT waived. You pay only the product’s MRP split into EMIs. However, note: Processing/GST charges may still apply (see next point).

- Dynamic Interest Rates: The rate is not fixed for all purchases. Always check the final transaction breakdown on the bill or app before confirming.

2. Processing Fee / Convenience Fee

Bajaj Finserv EMI Card Charges Details: This is one of the most common charges users encounter.

- What it is: A non-refundable fee charged to facilitate the EMI transaction. It covers administrative costs.

- When it’s Charged:

- On almost all No-Cost EMI transactions. While the interest is subsidized, a processing fee of 1-3% of the transaction value (plus 18% GST on the fee) is common.

- On regular EMI purchases, it may be bundled into the interest calculation or charged separately.

- Example: On a ₹30,000 No-Cost EMI purchase with a 2% processing fee:

- Processing Fee = 2% of ₹30,000 = ₹600

- GST (18%) on ₹600 = ₹108

- Total Deducted at Transaction = ₹708

- Your EMI will be calculated on ₹30,000, but your initial account ledger will show a debit of ₹708 as charges.

3. Foreclosure Charges

Bajaj Finserv EMI Card Charges Details: Want to close your EMI loan early? That attracts a cost.

- Charge: Typically, up to 4% of the principal outstanding amount, plus applicable GST.

- When it’s Charged: When you decide to repay the entire remaining loan amount before the original tenure ends.

- Logic: Lenders incur a loss on expected interest earnings. This charge compensates for that.

- Tip: Always calculate if the foreclosure charge is less than the future interest you would pay. Contact customer care for the exact foreclosure amount before proceeding.

4. Part-Payment Charges

Bajaj Finserv EMI Card Charges Details: Similar to foreclosure, but for paying off a portion of the outstanding.

- Charge: Usually, 2-4% of the part-payment amount, plus GST.

- When it’s Charged: When you pay a lump sum larger than your EMI to reduce your principal outstanding.

5. Late Payment Fees

Bajaj Finserv EMI Card Charges Details: Missing your EMI due date is costly and hurts your credit score.

- Charge: A penalty fee that varies, often ₹300 – ₹500 per missed EMI, plus GST.

- Impact: Beyond the fee, this can lead to a negative remark on your CIBIL report, affecting future loan eligibility.

6. Cheque/ECS/ Auto-Debit Bounce Charges

Bajaj Finserv EMI Card Charges Details: If your payment instrument fails, a penalty is levied.

- Charge: Usually between ₹300 – ₹500 per bounce, plus GST.

7. Duplicate Statement/ NOC Certificate Charges

Bajaj Finserv EMI Card Charges Details: Administrative document requests can have fees.

- Charge: Around ₹100 – ₹500 per request, plus GST, for physical copies or duplicate No Objection Certificates (NOCs).

8. Goods and Services Tax (GST)

Crucial Reminder: GST at 18% is applicable on almost all the above charges (processing fee, foreclosure fee, late payment fee, etc.). It is not a separate charge by Bajaj Finserv but a government-mandated tax on the service fee.

Part 3: Charges for Specific Features

1. EMI Card to Bank Account Transfer (Flexi Instant Loan Feature)

Bajaj Finserv EMI Card Charges Details: This feature allows you to transfer credit to your bank account for use at non-partner stores.

- Interest Rate: The interest rate for this cash transfer is generally higher than for standard product EMIs, often starting from 16% p.a. and going upwards.

- Processing Fee: A significant processing fee of 2-4% of the transferred amount (plus GST) is standard.

2. Charges on Accessing Credit Limit Information

Bajaj Finserv EMI Card Charges Details: Typically, checking your limit via app or portal is free. However, requesting detailed physical statements or specific documents might have nominal charges as mentioned above.

Part 4: How to Check Your Applicable Charges & Minimize Costs

1. The Golden Rule: Read the Transaction Slip.

Bajaj Finserv EMI Card Charges Details: Before signing any document at the store or clicking “Confirm” online, a detailed breakdown (Product Cost, Interest, Processing Fee, EMI Amount, Tenure) is provided. Scrutinize it.

2. Use the Bajaj Finserv App.

The app is transparent. For any transaction or loan, navigate to:

My EMI Card>My Loans> Select a Loan >View Loan Details. All fees, interest, and schedule are listed.

3. Minimizing Charges: Pro Tips

- Always Ask for “No-Cost EMI”: But explicitly ask, “Are there any processing fees on this no-cost EMI?”.

- Avoid Bank Transfers: The EMI card-to-account transfer is the most expensive feature. Use it only in necessity.

- Never Miss an EMI: Set reminders or enable auto-debit to avoid heavy late fees and credit score damage.

- Foreclose Wisely: Calculate if the foreclosure charge saves you money in the long run.

- Leverage Free Periods: Some transactions might offer a short interest-free period if converted to EMI later. Understand the terms.

- Shop During Festive Sales: Brands often offer genuine low-fee or zero-fee no-cost EMI during big sales.

Conclusion: Empowerment Through Knowledge

Bajaj Finserv EMI Card Charges Details: The Bajaj Finserv EMI Card is a potent instrument for managing cash flow and affording necessities without financial strain. Its true value is unlocked not just by using it, but by using it wisely. The charges are not meant to trap users but to cover operational risks and costs. By understanding the detailed breakdown of processing fees, foreclosure penalties, and the reality behind “no-cost” offers, you transform from a passive user to an empowered financial consumer.

Remember, if in doubt, the 24/7 customer care helpline and the transparent Bajaj Finserv app are your best allies. Informed spending is smart spending.

Frequently Asked Questions (FAQ)

Q1: Is the Bajaj Finserv EMI Card completely free to use?

Bajaj Finserv EMI Card Charges Details: A: While there is no annual fee, the card is not free to use. Costs are transaction-based. Standard EMI purchases incur interest, and even “No-Cost EMI” deals often have a processing fee (1-3% + GST). Other charges apply for late payments, foreclosures, etc.

Q2: Why was I charged a processing fee on a “No-Cost EMI” purchase?

Bajaj Finserv EMI Card Charges Details: A: “No-Cost EMI” means the interest is waived or subsidized by the brand. However, a processing or convenience fee is charged separately by the financier (Bajaj Finserv) to manage the transaction. This is a standard industry practice. Always check the cost breakdown before confirming.

Q3: What is the most expensive charge I should avoid at all costs?

Bajaj Finserv EMI Card Charges Details: A: Late Payment Fees are the most critical to avoid. They include a penalty (₹300-500 + GST), potentially high late payment interest, and most damagingly, a negative impact on your CIBIL credit score, which can affect future loan approvals for years.

Q4: How can I find out the exact charges for my specific transaction?

A: The details are always disclosed before final payment:

In-store: On the digital or physical transaction slip you sign.

Online: On the checkout page breakdown before the final “Pay” click.

Anytime later: In the “My Loans” section of the Bajaj Finserv app, under the specific loan details.

Q5: If I transfer my EMI Card limit to my bank account, what are the charges?

A: This “Flexi Loan” feature is among the costliest. It typically carries a higher interest rate (often from 16% p.a.) and a significant one-time processing fee of 2-4% of the transferred amount + GST. It should be used only for essential needs when other cheaper credit options are unavailable.